Thrive Blogs

Software Testing and QA Services Market The Software Testing and QA Services Market is estimated to be valued at US$ 38.42 Bn in 2023 and is expected to exhibit a CAGR of 13% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Software testing and QA services help organizations validate software products and applications to verify they function as per intended use cases. These services test software for functionality, usability, performance and reliability to ensure no glitches remain. With growing digital transformation across industries, software testing and QA services assume greater importance in delivering error-free software to end-users. Market key trends: The increasing adoption of automation testing solutions is a major trend in the software testing and QA services market. Automation testing helps test functionality and integration of applications faster by reducing dependence on manual testing. It allows for testing of applications across various platforms and browsers in parallel to traditional QA cycles. Various automation tools are available which can design, execute and generate reports of test results. These tools save significant time and cost for organizations compared to only manual testing. With complex software requiring extensive validation, demand for automation testing solution is poised to grow in the coming years. Porter's Analysis Threat of new entrants: New entrants face high initial costs to enter the market. They also need to gain customer trust and recognition to compete with established players. Bargaining power of buyers: Buyers have moderate bargaining power due to the presence of many vendors providing similar services. However, switching costs are low. Bargaining power of suppliers: Software testing service providers have low bargaining power as there are several freelancers and startups providing similar testing services. Threat of new substitutes: Threat from substitutes is low as software testing requires technical skills that are not easily replaceable. Competitive rivalry: High as the market comprises many global and regional players competing on factors like pricing, technical expertise and relationships. SWOT Analysis Strengths: Established global delivery model, strong domain knowledge, talented workforce. Weaknesses: Low switching costs, dependency on client budgets, pricing pressures. Opportunities: Growth in digital transformation, adoption of AI/ML, demand from verticals like Banking, Telecom. Threats: Economic slowdowns, protectionist regulations, visa restrictions. Key Takeaways The global software testing and QA services market is expected to witness high growth, exhibiting CAGR of 13% over the forecast period, due to increasing demand for testing in Agile/DevOps environments and adoption of test automation. The US market dominates currently due to large IT modernization programs. Asia Pacific is expected to grow at the fastest pace led by countries like India and China. India is a major outsourcing destination providing cost benefits for global enterprises. Key players operating in the software testing and QA services market are TCS, Wipro, Cognizant, Infosys, IBM, Qualitest, CGI, Mindtree, Cygnet Infotech, Maveric Systems, QA Mentor, A1QA, QA Source, QASource, Capgemini, Accenture, HCL Technologies, Atos, DXC Technology, Tech Mahindra. TCS and Wipro captured the largest market shares in 2021, whereas regional players like Maveric systems and QA Mentor are rapidly expanding. Read More: https://www.rapidwebwire.com/software-testing-market-estimated-to-witness-strong-growth-owing-to-growing-adoption-of-agile-methodologies-and-expanding-digital-transformation-initiatives/

0 Comments

Primary Care Physicians Market is Estimated To Witness High Growth Owing To Aging Population11/7/2023  Primary Care Physicians Market The Primary Care Physicians Market is estimated to be valued at US$ 701.20 billion in 2023 and is expected to exhibit a CAGR of 4.5% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Primary care physicians provide various medical services including diagnosis and treatment of both acute and chronic medical conditions, preventive care and management of routine healthcare needs across all ages. They are often the patient's first point of contact for health issues and play a key role in providing guidance regarding healthcare and medical management. Market key trends: One of the key trends fueling growth in the primary care physicians market is the aging population worldwide. As per the United Nations data, the number of people aged 65 years and above globally is projected to grow from 703 million in 2019 to 1.5 billion in 2050. Older individuals require more frequent medical care and management of chronic conditions. This substantially increases the patient volume and workload of primary care physicians. Additionally, an aging demographic signifies a higher prevalence of chronic diseases such as diabetes, cancer, heart disease, which necessitates continuous medical supervision and care provided by primary care doctors over long periods of time. Therefore, the growing geriatric population base worldwide presents immense opportunities in the long run for players operating in the primary care physicians market. Porter’s Analysis Threat of new entrants: The primary care physicians market requires substantial capital investment for medical education and compliance with regulatory standards which acts as a barrier for new entrants. Bargaining power of buyers: Individual patients have low bargaining power due to inelastic demand for primary care services and lack of transparency in pricing. However, large insurance companies have significant bargaining power to negotiate prices. Bargaining power of suppliers: Physicians have considerable bargaining power as the shortage of primary care doctors. Suppliers can choose facilities offering higher compensation. Threat of new substitutes: Some services offered by retail clinics, telehealth, and AI-based diagnostics pose a threat but cannot fully replace in-person primary care services. Competitive rivalry: Intense as physicians and hospitals compete for patients in local catchment areas. SWOT Analysis Strengths: Established brand reputation and customer loyalty for top healthcare providers. Integrated healthcare delivery networks allow for coordinated care. Weaknesses: Rising costs, medical errors, shortage of primary care physicians leads to scheduling delays. Large hospitals focus more on specialty services over primary care. Opportunities: Growing geriatric population driving demand for primary and preventive care services. Shift towards value-based models from fee-for-service. Threats: Economic slowdowns reduce individuals' ability to pay. Stringent regulations around pricing, quality, and access. Growing data privacy and security concerns. Key Takeaways The global primary care physicians market size is expected to witness high growth, exhibiting CAGR of 4.5% over the forecast period, due to increasing prevalence of chronic diseases and rising healthcare expenditure. The US dominates the global market, valued at US$ 701.20 billion in 2023 owing to large population and higher healthcare spending compared to other nations. The Asia Pacific region is poised to be the fastest growing market for primary care physicians due to growing medical tourism, rising income levels, increasing healthcare infrastructure and expanding health insurance coverage in major economies like China and India. Key players operating in the primary care physicians market include Mayo Clinic, Cleveland Clinic, Kaiser Permanente, Johns Hopkins Medicine, Massachusetts General Hospital, UCLA Health, Ascension, Providence St. Joseph Health, Rush University Medical Center, NewYork-Presbyterian, UCSF Health, Northwestern Medicine, Partners HealthCare, Mount Sinai Health System, University of Michigan Health System, University of Washington Medicine, Cedars-Sinai, Stanford Health Care, NYU Langone Health, Penn Medicine. These players are focusing on expanding service offerings and geographic presence through mergers and acquisitions. Read More: https://www.rapidwebwire.com/primary-care-physicians-market-estimated-to-witness-growth-owing-to-rising-healthcare-costs-and-growing-geriatric-population/  The Laboratory Proficiency Testing Market is estimated to be valued at US$ 1.29 billion in 2023 and is expected to exhibit a CAGR of 7.3% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Laboratory proficiency testing involves evaluating the performance of laboratories for quality assessment against ISO standards and accreditation criteria. It is essential for clinical, biomedical, and food testing laboratories to participate in proficiency testing programs on a regular basis to ensure test accuracy and precision as per quality management standards. Proficiency testing programs evaluates laboratories' competency in performing analytical testing of various biomarkers, microbes, chemicals, and other substances. Market key trends: Stringent regulations mandating clinical laboratory accreditation and quality assessment along with rising incidences of laboratory errors drive the demand for proficiency testing programs globally. In recent years, regulatory agencies across various countries have strengthened laboratory quality standards and mandated proficiency testing participation periodically for obtaining accreditation. Laboratories are now required to participate and clear proficiency testing challenges measuring competency on a regular frequency ranging from semi-annually to annually depending on the tests performed. This has boosted the adoption of external quality assessment solutions for ensuring test reliability and validity. Furthermore, growing focus on improving patient safety through error minimization is propelling healthcare facilities to embrace robust quality control practices including proficiency testing. Porter’s Analysis Threat of new entrants: Medium, capital requirement is moderately high for setting up testing facilities and obtaining accreditation which acts as a barrier for new players. Bargaining power of buyers: Moderate, buyers have bargaining power due to availability of testing facilities from various players but switching costs act as a constraint. Bargaining power of suppliers: Low, suppliers of testing equipment and raw materials have low bargaining power due to standardized nature and availability of substitutes. Threat of new substitutes: Low, no major substitute options available for proficiency testing services. Competitive rivalry: High, major players compete intensely on parameters such as quality, pricing, services and innovation. SWOT Analysis Strength: Established market presence of major players, strong technical expertise. Weakness: High capital requirement, complex regulatory approvals and certifications. Opportunity: Growth in biopharma outsourcing, increasing R&D spending. Threats: Price wars among players, stringent quality standards. Key Takeaways The laboratory proficiency testing market is expected to witness high growth, exhibiting CAGR of 7.3% over the forecast period, due to increasing R&D activities in pharmaceutical and biotech industries. North America dominates the market currently due to presence of major pharmaceutical companies. Europe is the second largest market. The Asia Pacific market is expected to grow at the fastest rate during the forecast period due to expanding biopharma industry and increasing healthcare spending in countries such as China and India. Key players operating in the Laboratory Proficiency Testing market are Bio-Rad Laboratories, LGC Limited, Merck KGaA, Randox Laboratories, Thermo Fisher Scientific, Westgard QC, Advanced Analytical Solutions, LLC, AOAC International, Bipea, CAP, Charmex, Fera Science Limited (Fera), Finning UK & Ireland, Helena Laboratories, Hygiena, International Education and Research Corporation (ERC), Maine Molecular Quality Controls, Inc. (MMQCI), Microbiologics, Inc., NSI Lab Solutions, QACS Ltd. Read More: https://www.rapidwebwire.com/laboratory-proficiency-testing-market-driven-by-growth-owing-to-rising-emphasis-on-quality-assurance-and-accreditation/  Nasal Vaccines Market The Nasal Vaccines Market is estimated to be valued at US$ 416.8 million in 2023 and is expected to exhibit a CAGR of 8.6% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

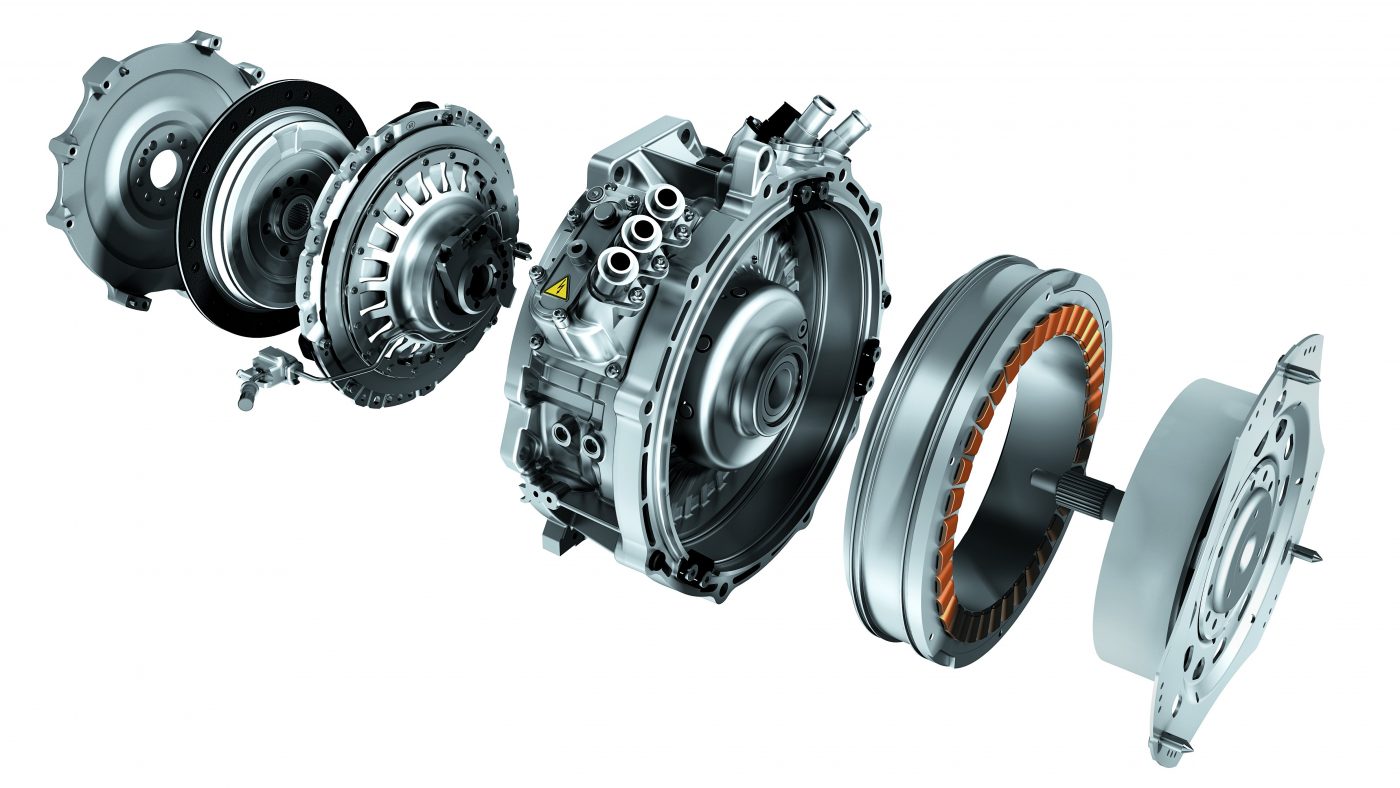

Market Overview: Nasal vaccines employ intranasal route of administration for vaccines, where the antigen is directly deposited in nasal mucosa, inducing both systemic and local immunity. Compared to injectable vaccines, nasal vaccines offer advantages such as needle-free administration, thermostability, and induction of both mucosal and systemic immunity. The need for alternative routes of vaccine administration has been rising in order to address the challenges of injection-based immunization. Market key trends: One of the key trends fueling the growth of the nasal vaccines market is the increased uptake of alternative routes for vaccine administration. The nasal route offers distinct advantages over injectable vaccines such as needle-free, painless administration, which increases patient compliance. Nasal vaccines also induce both systemic and mucosal immunity, activating immune responses at the site of pathogen entry. This provides superior protection against respiratory pathogens such as influenza. Furthermore, nasal vaccines are stable at room temperature, eliminating the need for cold chain transportation and storage. This facilitates easy stockpiling and administration of nasal vaccines in developing regions, thus supporting the scaling up of vaccination programs. Porter's Analysis Threat of new entrants: New entrants face high costs associated with R&D, clinical trials, regulatory approvals and manufacturing facilities to produce nasal vaccines. This poses significant barriers. Bargaining power of buyers: Nasal vaccine buyers include hospitals, clinics, government institutions and individuals. Their bargaining power is moderate due to availability of substitute treatment options. Bargaining power of suppliers: Key raw material suppliers face moderate bargaining power due to established supply networks of major players and differentiated products. Threat of new substitutes: Threat is low as nasal vaccines effectively target respiratory infections with non-invasive route of administration compared to injectable vaccines. Competitive rivalry: Intense as major players compete on pricing, innovation and marketing. SWOT Analysis Strengths: Nasal route bypass IV administration. Non-invasive self-administration improves patient compliance. Weaknesses: Require stringent temperature controls during storage and transport. High development costs associated with ensuring thermostability. Opportunities: Growing preference for needle-free vaccines. Rising incidence of respiratory infections globally. Threats: Stringent regulatory approvals. Reimbursement challenges in certain regions. Key Takeaways The global nasal vaccines market is expected to witness high growth, exhibiting CAGR of 8.6% over the forecast period, due to increasing prevalence of respiratory diseases globally. The US market currently dominates with a share of over 30% in 2023 due to presence of advanced healthcare infrastructure and major players. However, Asia Pacific region is expected to grow at fastest rate due to large patient pool, improving access and rising disease awareness in populous countries like India and China. Key players operating in the Nasal Vaccines market are AstraZeneca, GlaxoSmithKline plc, Pfizer Inc., Serum Institute of India Pvt. Ltd., Sanofi Pasteur SA, Johnson & Johnson Services, Inc., Sinovac Biotech Ltd., Bharat Biotech International Limited, Altimmune, Inc., BiondVax Pharmaceuticals Ltd., FluGen Inc., Vaxart, Inc., Intravacc, Ennaid Therapeutics, LLC, Gamma Vaccines Pty Ltd. The major players are focusing on product launches, collaborations and technology advancements to strengthen their market position. Read More: https://www.rapidwebwire.com/nasal-vaccines-market-estimated-to-witness-high-growth-owing-to-increased-disease-prevention-capabilities-and-growing-focus-on-drug-delivery-product-innovation/  Electric Motor Core Market The Electric Motor Core Market is estimated to be valued at US$ 18.97 billion in 2023 and is expected to exhibit a CAGR of 8.4% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: An electric motor core is an integral part of an electric motor which functions as a magnetic circuit and is used to produce torque. It provides a low reluctance path for magnetic flux and helps in aligning the magnetic lines of flux in the rotor and stator. Electric motor cores are made from soft magnetic materials like silicon steel to reduce the reluctance. They come in different shapes and sizes depending upon the type and application of electric motors. Market key trends: One of the major trends driving the growth of the electric motor core market is the rising adoption of renewable energy sources globally. Electric motors are used in various renewable energy systems like wind turbines, hydroelectric power generators etc. to convert energy into rotational mechanical power. With renewable energy becoming more cost competitive and governments pushing clean energy initiatives, demand for electric motors from renewable sources is expected to increase significantly over the coming years. This will augment the demand for electric motor cores from renewable energy applications. Additionally, technological advancements to improve motor efficiency through better core material and designs is also fueling market growth. Porter's Analysis Threat of new entrants: Low capital requirements and established buyers limit threat of new entrants. Bargaining power of buyers: Large buyers have significant influence on pricing due to high bargaining power. Bargaining power of suppliers: Few component suppliers exist with differentiated products, increasing supplier power. Threat of new substitutes: Limited substitute products exist currently, though technology advancement may introduce novel alternatives. Competitive rivalry: Intense competition exists among dominant industry players to gain market share. SWOT Analysis Strengths: Established brand names, proprietary technologies, and global distribution networks. Weaknesses: High research and development costs, regulatory compliance complexities. Opportunities: Expanding into emerging markets, potential for acquisitions, partnerships and licensing agreements. Threats: Price erosion, healthcare reforms and legislation, intellectual property challenges. Key Takeaways The electric motor core market is expected to witness high growth, exhibiting CAGR of 8.4% over the forecast period, due to increasing adoption of electric vehicles globally. The Asia Pacific region dominates the global market currently and is expected to maintain its leading position over the forecast period due to presence of key players and rapidly growing end-use industries in China and India. By product, the rotor segment accounted for the largest share of the global market in 2023. Rotors make up the magnetic circuit of an electric motor that produces torque and are a critical component for motor functioning. Regional analysis - North America is forecast to witness significant growth due to increasing investments by leading players to expand their presence. Presence of developed healthcare infrastructure and rising musculoskeletal disorders in the US and Canada also support growth. Key players operating in the Electric Motor Core market are Johnson & Johnson (DePuy Synthes), Medtronic plc, Stryker Corporation, Zimmer Biomet Holdings, Inc., Smith & Nephew plc, NuVasive, Inc., Globus Medical, Inc., Wright Medical Group N.V., Arthrex, Inc., DJO Global, Inc., Össur hf., CONMED Corporation, Breg, Inc., Orthofix Medical Inc., Bioventus LLC. Read More: https://www.rapidwebwire.com/the-electric-motor-core-market-estimated-to-witness-significant-growth-due-to-rising-investment-in-renewable-energy-growing-electric-vehicle-industry/  The Disposable Face Mask Market is estimated to be valued at US$ 44.72 Bn in 2022 and is expected to exhibit a CAGR of 10.2% over the forecast period 2023 to 2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Disposable face masks are widely used as preventive care for airborne diseases. It acts as a physical barrier between the mouth and nose of wearer and potential contaminants in the immediate environment. Disposable face masks are made up of non-woven fabric such as polypropylene and come with elastic ear loops. They are used by people during severe air pollution, dust, smoke or when sick to prevent spreading of germs. Market Dynamics: The disposable face mask market is primarily driven by growing awareness among people about airborne diseases such as influenza, swine flu and COVID-19 pandemic. People are increasingly opting for disposable masks as they provide adequate protection against airborne pathogens. Moreover, increased preference for disposable products over reusable masks owing to convenience factors is also boosting the market growth. Geographically, Asia Pacific dominates the global disposable face mask market and is expected to retain its dominance over the forecast period owing to rising industrialization and urbanization leading to high air pollution levels in the region. Here is the SWOT Analysis and Key Takeaways without conclusion as per your instructions: SWOT Analysis Strength: Disposable face masks are convenient and affordable. They are easily accessible and mass produced which keeps the costs low. They effectively filter out particles in the air and prevent spread of infections. Weakness: Disposable face masks are not reusable and produce non-biodegradable waste. Frequent disposal increases environmental footprint. The fittings are not customized for different face sizes. Opportunity: Growing awareness about health, hygiene and air pollution control is driving the demand for face masks. Stringent regulations mandating the use of masks will boost market revenues. Threats: Alternatives like reusable cloth masks pose competition. Economic slowdowns can impact discretionary spending on face masks. Key Takeaways The global disposable face mask market is expected to witness high growth, exhibiting CAGR of 10.2% over the forecast period, due to increasing awareness about health, hygiene and air pollution control. Regional analysis: North America dominates the global disposable face masks market currently. The region accounts for over 30% market share due to strict regulations regarding infection control and worker safety in several industries. Asia Pacific exhibits the fastest growth led by China, India and other developing nations. Rising income levels and public health initiatives are propelling the regional market. Key players: Key players operating in the disposable face mask market are Kimberly-Clark, 3M Company, uvex group, The Gerson Company, Kowa Company Ltd., Moldex-Metric Inc., Bunzl PLC (SAS Safety Corp.), and Honeywell International Inc., among others. Companies are focusing on manufacturing medically approved masks and expanding production capacities to fulfill the surging demand. Read More: https://www.ukwebwire.com/asia-pacific-disposable-face-mask-market-to-exhibit-substantial-growth-over-the-next-decade/  Construction Chemicals Market The Construction chemicals Market is estimated to be valued at US$ 49.9 billion in 2022 and is expected to exhibit a CAGR of 6% over the forecast period 2023 to 2032, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Construction chemicals are chemical formulations that enhance the quality and strength of construction materials and structures by protecting or strengthening them. These chemicals are used at different stages of construction from pre-construction to post-construction. Admixtures, protective coatings, adhesives, sealants, and concrete repair & rehabilitation products are some examples of construction chemicals. They enhance the durability and lifespan of structures by protecting them from corrosion, moisture and cracks. Market key trends: Infrastructure development in emerging economies is a key driver for growth of the construction chemicals market. Rapid urbanization and growing populations are increasing demand for residential, commercial and industrial construction, which requires large amounts of construction chemicals. Governments across India, China, Indonesia and other Asian countries are investing heavily in infrastructure projects like roads, bridges, airports and other public structures. This is fueling consumption of various construction chemicals like concrete admixtures, adhesives, protective coatings and repair compounds. The construction chemicals market is expected to continue growing steadily with increasing investment in infrastructure globally over the forecast period. Porter’s Analysis: Threat of new entrants: The threat of new entrants is moderate as the construction chemicals market requires large capital investments and established distribution channels. However, the industry experiences steady growth providing opportunities for new players. Bargaining power of buyers: The bargaining power of buyers is high given the fragmented nature of the industry with numerous local and regional construction chemical providers. Buyers can negotiate on price and quality. Bargaining power of suppliers: The bargaining power of suppliers is moderate as key raw materials for construction chemicals like resins and polymers have few substitutes and suppliers. However, established players can source from multiple suppliers. Threat of new substitutes: The threat of substitutes is low as construction chemicals have few product substitutes that provide the same functionalities of adhesion, waterproofing etc. Competitive rivalry: Intense competition. SWOT Analysis: Strengths: Wide product portfolio and presence across regions. Established brands and technical expertise. Weaknesses: Vulnerable to fluctuations in raw material prices. High customer acquisition and retention costs. Opportunities: Growing infrastructure and real estate development worldwide. Shift towards green buildings provides opportunities. Threats: Stringent regulations regarding VOCs and hazardous chemicals. Economic slowdowns negatively impact demand. Key Takeaways: The global construction chemicals market size is expected to reach $49.9 billion in 2022, exhibiting a CAGR of 6% during the forecast period. Rapid urbanization and the rise of mega cities around the world is driving demand for new residential and commercial construction. The commercial segment dominates currently due to rising investments in hotels, malls and office spaces. Regionally, Asia Pacific dominates the construction chemicals market currently and is projected to continue its lead, growing at over 7% annually till 2032. This can be attributed to the robust expansion of the residential and infrastructural construction industries in China and India. Western Europe and North America are also sizable markets driven by renovation and refurbishment activities. Key players operating in the construction chemicals market are Pidilite Industries, BASF SE, RPM International Inc., Sika A.G., The Dow Chemical Company, Fosroc International, Arkema S.A., Ashland Inc., Mapei S.p.A, and W.R. Grace. These leading vendors dominate through extensive R&D and new product launches catering to evolving construction requirements like green buildings. Read More: https://www.rapidwebwire.com/construction-chemicals-market-estimated-to-witness-exponential-growth/  The Africa Bitumen Market is estimated to be valued at US$ 418.71 Mn in 2020 and is expected to exhibit a CAGR of 5.3% over the forecast period from 2021 to 2028, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Bitumen is a semi-solid form of petroleum which is highly viscous and can be moldable. It is used in various construction applications such as road construction and waterproofing. The increasing infra development activities across the region are fueling the demand for bitumen in Africa. Market key trends: One of the major trends driving the growth of Africa bitumen market is increasing investments in road infrastructure projects. Various countries in Africa such as Nigeria, South Africa, Kenya etc. are investing heavily in development and upgrading of road networks. For instance, Nigeria government has planned to invest around US$ 2.7 billion over the next 3 years to construct and rehabilitate nearly 13,000 kilometers of federal roads across the country. Such increasing focus on infra development is expected to significantly boost the consumption of bitumen in road construction activities in Africa over the forecast period. Porter’s Analysis Threat of new entrants: Low barrier of entry in bitumen market in Africa due to availability of raw material. However, established players have advantage of brand name and distribution channels. Bargaining power of buyers: Buyers have moderate bargaining power due buyers like road construction companies have limited alternatives for bitumen. Bargaining power of suppliers: Suppliers have moderate power due to availability of raw material reserves from a few suppliers globally. However, production capacity expansion can impact prices. Threat of new substitutes: Limited threat as bitumen has well established applications and no cost effective substitutes available for usage in roads construction. Competitive rivalry: High due to presence of petroleum companies and construction material suppliers competing on pricing and quality. SWOT Analysis Strength: Availability of crude oil reserves and investments in refining assets by key players. Rising road infrastructure projects provide increased demand. Weakness: High dependence on imports to meet demand-supply gap. Vulnerable to volatility in crude oil prices. Lack of local manufacturing capacity. Opportunity: Growing population and urbanization driving road construction activities. Government focus on upgrading transport infrastructure offers scope. Threats: Economic and political instability in certain African countries pose project delays. Rising competition from alternatives like cement for construction. Key Takeaways The Africa bitumen market is expected to witness high growth, exhibiting CAGR of 5.3% over the forecast period, due to increasing road construction activities across the region. The fastest growing regional market is expected to be East Africa registering a CAGR of over 6% primarily due to rising infrastructure projects in countries like Ethiopia, Kenya and Tanzania. Key players operating in the Africa bitumen market are Exxon Mobil Corporation, Royal Dutch Shell Plc., RAHA Bitumen, Inc., Tekfalt Binders (Pty) Ltd., SprayPave, Indian Oil Corporation Ltd., GOIL Company Limited, Wabeco Petroleum Ltd., Tiger Bitumen, and Richmond Group. Exxon Mobil captured around 25% market share in 2020 owing to huge reserves and supply contracts with major construction companies. Regional analysis indicates East Africa as the fastest growing market for bitumen consumption particularly in Ethiopia, Kenya and Tanzania. This is attributed to rising FDI inflows for transportation projects under China’s Belt and Road Initiative. The governments growing focus on upgrading road networks to support trade and economic growth bodes well. Read More: https://www.rapidwebwire.com/africa-bitumen-market-is-estimated-to-witness-high-growth-owing-to-growing-road-infrastructure-development/  India Advanced Wound Care Management Market The India advanced wound care management market is estimated to be valued at US$ 281.1 million in 2022 and is expected to exhibit a CAGR of 5.1% over the forecast period 2022-2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: Advanced wound care products are innovative wound healing products that help manage complex and chronic wounds related to leg ulcers, pressure ulcers, and surgical and traumatic wounds among others. These products prevent infections, manage excess fluid from the wound, and maintain a moist wound environment that promotes healing. The growing geriatric population suffering from diabetes and pressure ulcers has increased the need for advanced wound care products in India. Market key trends: The rising prevalence of diabetes is a major driver of growth in the Indian advanced wound care management market. As per the International Diabetes Federation (IDF), India has the second-highest number of diabetic patients in the world with approximately 77 million cases in 2019. Untreated diabetes leads to various complications including foot ulcers that require advanced treatment. Wounds related to diabetes accounted for over 40% of the total wound management expenditure in India in 2021. Advanced wound care products that help manage acute and chronic diabetic foot ulcers effectively are gaining increased adoption to reduce healthcare costs associated with amputations and hospitalizations. Porter’s Analysis Threat of new entrants: Low capital requirements and established brand recognition of existing players create significant barriers for new entrants. Bargaining power of buyers: Relatively high number of product options provides buyers with bargaining power to demand competitive pricing. Bargaining power of suppliers: Established supply networks of key players reduce suppliers’ ability to influence prices. Threat of new substitutes: Alternate advanced wound care options pose threat of substitution. Competitive rivalry: Intense competition among existing players. SWOT Analysis Strengths: Growing geriatric population prone to chronic wounds and emergence of advanced products boost market growth. Weaknesses: High cost of advanced treatments limits widespread adoption. Lack of reimbursement policies in developing regions hampers market revenues. Opportunities: Rising incidence of diabetes and associated complications widen opportunities. Growing awareness about available treatment alternatives fuels demand. Threats: Limited healthcare spending and strong presence of conventional treatment methods restrict market growth. Key Takeaways The India advanced wound care management market is expected to witness high growth, exhibiting CAGR of 5.1% over the forecast period, due to increasing prevalence of chronic diseases such as diabetes. Rising cases of diabetes related foot ulcers and diabetic foot wounds in India propel market revenues. Regionally, southern India dominates the market and is estimated to grow at the fastest rate during the analysis period owing to rising healthcare standards. Western India also offers lucrative opportunities due to presence of leading medical facilities in major cities. Key players operating in the India Advanced Wound Care Management market are Smith and Nephew Plc, Coloplast A/S, Johnson and Johnson, 3M, Convatec Group Plc, Cologenesis Healthcare Pvt Ltd, Mil laboratories Pvt Ltd, Essity AB, Eucare Pharmaceuticals Ltd. Major players focus on bringing advanced product variants and expanding access to rural markets through new partnerships. Read More: https://www.rapidwebwire.com/india-advanced-wound-care-management-market-estimated-to-witness-growth/ Increasing Demand For OEM And Aftermarket Parts to Drive the ASEAN Automotive Aftermarket Growth11/1/2023  ASEAN automotive aftermarket The ASEAN Automotive Aftermarket Market is estimated to be valued at US$ 28.7 Bn in 2023 and is expected to exhibit a CAGR of 9.8% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights.

Market Overview: The ASEAN Automotive Aftermarket includes replacement parts, accessories, tires, batteries, lubricants, window films, and other components that are required for repair, maintenance, or upgrade of the vehicles in the region. Automotive parts are required for regular maintenance and repair of vehicles to ensure smooth functioning and extend the lifespan of vehicles. The increasing average age of vehicles and rising vehicle parc has driven the demand for OEM and aftermarket parts in the ASEAN region. Market key trends: The ASEAN Automotive Aftermarket is witnessing high growth owing to the increasing demand for OEM and aftermarket parts. The average age of vehicles in ASEAN countries has been steadily increasing over the past few years and stood at around 9-10 years in major countries like Thailand, Indonesia, and Malaysia in 2023. As vehicles age, the requirement of replacement parts and maintenance increases. This has boosted the demand for OEM parts that are designed to original specifications as well as compatible and affordable aftermarket parts. The increasing vehicle parc in the ASEAN region coupled with rising disposable income has also augmented the demand for vehicle accessories and cosmetic upgrades, thereby fueling the growth of the aftermarket. Porter's Analysis Threat of new entrants: Low capital requirements and established suppliers pose low threat of new entrants. However, high competition and customer loyalty towards established brands act as a barrier. Bargaining power of buyers: Buyers have high bargaining power due to availability of substitutes and undifferentiated products. Switching costs are relatively low. Bargaining power of suppliers: Parts suppliers possess moderate bargaining power due to differentiated products and availability of substitute parts from other suppliers. Threat of new substitutes: Threat of substitutes is moderate as original equipment manufacturers continue to focus on technology advancement. Competitive rivalry: Industry comprises global and regional players, leading to high competitive rivalry. SWOT Analysis Strength: Wide product portfolio and extensive distribution network of key players. Growing demand for vehicle maintenance and aftermarket parts. Weakness: High dependency on economic conditions and disposable income of customers. Supply chain disruptions affect timely delivery. Opportunity: Increasing vehicle parc and rapid urbanization in developing nations. Shift towards online sales channels to boost connectivity. Threats: Stringent environmental regulations regarding carbon emissions. Trade wars and geopolitical tensions impact profit margins. Key Takeaways The global ASEAN automotive aftermarket is expected to witness high growth, exhibiting CAGR of 9.8% over the forecast period, due to increasing vehicle parc in Southeast Asia. Growing middle-class population and rising disposable income fuel vehicle sales. Regional analysis- The Indonesia automotive aftermarket dominates the ASEAN region with a size of over US$ 7 Bn in 2023 owing to large vehicle fleet. Countries like Vietnam, Thailand, and Malaysia exhibit higher growth prospects supported by Government initiatives to boost automotive manufacturing. Key players operating in the ASEAN automotive aftermarket are Bridgestone Corporation, Denso Corporation, Hella KGaA, BorgWarner Inc., Robert Bosch GmbH, Continental AG, Enkei Corporation, F.C.C. Co.,Ltd., Mitsuba Corp., Schlemmer, Showa Corporation, Yachio Industry Co., Ltd., TOYOTA MOTOR CORPORATION, and ZF Friedrichshafen AG. These players focus on expanding distribution networks and new product launches catering to local automotive needs. Read More: https://www.rapidwebwire.com/the-asean-automotive-aftermarket-is-estimated-to-witness-high-growth-owing-to-rising-vehicle-parc/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

November 2023

Categories

All

|

RSS Feed

RSS Feed